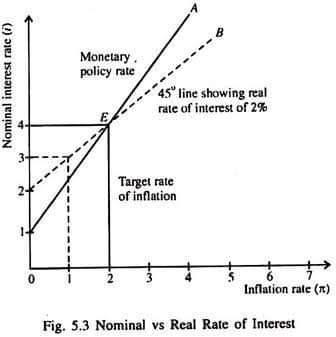

The Fisher equation expresses the relationship between nominal interest rates and real interest rates under inflation. Named after Irving Fisher, an American economist, it can be expressed as real interest rate ≈ nominal interest rate − inflation rate.

In more formal terms, where r equals the real interest rate,

i equals the nominal interest rate, and π equals the inflation rate, the Fisher equation is

r = I – π

It can also be expressed as ;

(1 + i) = (1 + r)(1 + π)

✓ Let’s consider an application of the Fisher equation in the context of borrowing. Suppose you want to take out a loan for $10000 with a nominal interest rate of 5% per year. If the expected inflation rate is 2% per year we can use the Fisher equation to calculate the real interest rate.

Nominal Interest Rate = Real Interest Rate + Inflation Rate

5% = Real Interest Rate + 2%

To isolate the real interest rate we subtract 2% from both sides of the equation:

5% – 2% = Real Interest Rate

Therefore the real interest rate is 3%.

This means that after adjusting for inflation the real interest rate on the loan is 3%. So if inflation remains at 2% per year you would need to earn a return of at least 3% on your investment or project to be able to repay the loan and still make a profit.

On the other hand if you were a lender the Fisher equation would help you determine the nominal interest rate to charge on the loan to ensure you are adequately compensated for the real interest rate and expected inflation. By adjusting the nominal interest rate based on inflation expectations lenders can protect their purchasing power and ensure a fair return on their lending.

In summary the Fisher equation is a useful tool to analyze the impact of inflation on borrowing and lending. It allows borrowers and lenders to consider the real interest rate and adjust for inflation to make informed financial decisions.